|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The growth in securities lending transactions, such as securities loans and repurchase agreements, has been such in recent years that they now represent a substantial part of the daily settlement value in many settlement systems and play an important role in facilitating market liquidity. It is expected that securities lending activity will continue to increase as an integral part of contemporary securities markets.

The growth in securities lending transactions, such as securities loans and repurchase agreements, has been such in recent years that they now represent a substantial part of the daily settlement value in many settlement systems and play an important role in facilitating market liquidity. It is expected that securities lending activity will continue to increase as an integral part of contemporary securities markets.

Securities lending involves the temporary exchange of securities, generally for cash or other securities of at least an equivalent value, with an obligation to redeliver a like quantity of the same securities on a future date.

There two types of securities lending transactions: "securities-driven" and "cash-driven". Broadly, in "securities-driven" transactions, institutions seek to lend/borrow specific securities against collateral, while in "cash-driven" transactions; institutions seek to lend/borrow securities as collateral in cash financing arrangements.

There two types of securities lending transactions: "securities-driven" and "cash-driven". Broadly, in "securities-driven" transactions, institutions seek to lend/borrow specific securities against collateral, while in "cash-driven" transactions; institutions seek to lend/borrow securities as collateral in cash financing arrangements.

We, IFC, provide the lending of securities to other parties who may sell them short or use them to satisfy some other obligation to deliver those particular securities to another party.

In return for lending available securities, we as lenders representatives receive a fee that may amount to a few basis points a year.

Our loaned securities are typically collateralised. This reduces our credit exposure to the borrower. The lender, however, retains the market risk of loaned securities. This is because the borrower is obligated to ultimately return the securities—not the original market value of the securities—to the lender.

Collateralisation is a means of reducing credit exposure to a counterparty. Under a collateralisation arrangement, a party who owes an obligation to another party posts collateral—typically consisting of cash or securities—to secure the obligation. In the event that the party defaults on the obligation, the secured party may seize the collateral. Collateral is sometimes called "margin."

Collateral is used in a variety of situations, including foreign exchange forwards, securities lending and derivatives transactions. An arrangement can be unilateral with just one party posting collateral. With two-sided obligations, such as a swap or foreign exchange forward, bilateral collateralisation may be used. In that situation, both parties may post collateral for the value of their total obligation to the other. Alternatively, the net obligation may be collateralised—at any point in time, the party who is the net obligator posts collateral for just the value of the net obligation.

![]() In a typical collateral arrangement, the secured obligation is periodically marked-to-market, and the collateral is adjusted to reflect changes in value. The securing party posts additional collateral when the market value has risen, or removes collateral when it has fallen.

In a typical collateral arrangement, the secured obligation is periodically marked-to-market, and the collateral is adjusted to reflect changes in value. The securing party posts additional collateral when the market value has risen, or removes collateral when it has fallen.

A typical collateral agreement should specify:

1. Acceptable collateral: A secured party will usually prefer to receive highly rated collateral such as Treasuries or agencies. Collateral whose market value is volatile or negatively correlated with the value of the secured obligation is generally undesirable.

2. Frequency of margin calls: Because both the value of an obligation and the value of posted collateral can change over time, a secured party typically wants to mark-to-market frequently, issuing a "margin call" to the securing party for additional collateral when needed.

3. Haircuts: In determining the amount of collateral that must be posted, haircuts are applied to the market value of various types of collateral. For example, if a 1% haircut is applied to Treasuries, then Treasuries are valued at 99% of their market value. A 5% haircut might be applied to certain corporate bonds, etc.

4. Threshold level: Only the value of an obligation above a certain threshold level may be collateralised. For example, if a $1MM threshold applies to a $5MM obligation, only $4MM of the obligation will actually be collateralised.

5. Close-out and termination clauses: The parties must agree under what circumstances the obligation will be terminated. The form of a final settlement in the event of such termination—and the role of the collateral in such settlement—is specified.

6. Valuation: A methodology for marking both the obligation and the collateral to market must be agreed upon.

7. Rehypothecation rights: The secured party may wish to have use of posted collateral—possibly lending it to another party or posting it as collateral for its own obligations to another party. Rehypothecation is not permitted in many jurisdictions.

Treatment of collateral varies from one legal jurisdiction to another. In some jurisdictions, the secured party takes legal possession of collateral, but is legally bound by how the collateral may be used and the conditions upon which it must be returned. Such transfer of title provides the secured party a high degree of assurance that it may seize the collateral in the event of a default. Transfer of title, however, may be treated as a taxable event in some jurisdictions. In other jurisdictions, the securing party retains ownership of collateral, but the secured party has a "perfected" interest in it.

Market overview

1 Introduction to securities lending markets

In today’s capital markets, securities seldom lie idle. If not being bought and sold in outright market transactions, securities are frequently lent to parties wanting to borrow them, or used as collateral to raise short-term finance. These transactions include repurchase agreements (repos), securities loans and sell-buyback agreements. While they differ in detail, they nonetheless have many similarities.1 This report treats them as a family of transactions, generically described as “securities lending”. Securities lending has become a central part of securities market activity in recent years, to a point where the daily volume of securities transactions for financing purposes considerably exceeds that of outright purchase and sale transactions.

Securities lending involves the temporary exchange of securities, usually for other securities or cash of an equivalent value (or occasionally a mixture of cash and securities), with an obligation to redeliver a like quantity of the same securities at a future date. Most securities lending is structured to give the borrower legal title to the securities for the life of the transaction, even though, economically, the terms are more akin to a loan. The borrow fee is generally agreed in advance and the lender has contractual rights similar to beneficial ownership of the securities, with rights to receive the equivalent of all interest payments or dividends and to have equivalent securities returned. The importance of the transfer of legal title is twofold. First, it allows the borrower to deliver the securities onward, for example in another securities loan or to settle an outright trade. Second, it means that the lender usually receives value in exchange for the disposition of legal title (whether in cash or securities), which ensures that the loan is collateralised.

1.1 Securities-driven and cash-driven markets

1.1 Securities-driven and cash-driven markets

While the securities lending markets can be broadly defined to include a range of transactions where there is a temporary transfer of securities, they actually comprise two, somewhat distinct markets: one that is “securities-driven” and one that is “cash-driven”.

In the securities-driven market firms seek to gain temporary access to specific securities. This may be because they have failed to receive securities that they are due to make delivery on or because they have deliberately sold a security short and are using the loan to deliver against this position.2 The securities borrower will usually give collateral to the lender. This may be in the form of other securities, cash or a bank letter of credit. Collateral mitigates the lender’s exposure to credit risk on the borrower.

In the cash-driven market, firms post securities as collateral to obtain cash financing. The cash lender is not seeking specific securities and will generally allow the cash borrower to select within defined categories of “general collateral”, for instance all domestic government securities issues. Market participants use these transactions to finance their portfolios at rates generally below the interbank short-term uncollateralised lending rate.

In both the cash-driven and the securities-driven markets, any margin is usually provided by the giver of collateral – in other words, the market value of collateral should exceed that of the cash or securities loaned. Thus, in the cash-driven market, margin gives a measure of protection against adverse movements in market prices to the cash lender and, in the securities-driven market; it protects the securities lender against non-delivery.

Traditionally, certain transaction structures have been associated with particular markets – for nstance, many countries’ cash-driven securities lending markets are structured through repos, typically of government debt, whereas securities-driven markets are structured as securities loans, typically of equities. However, in most jurisdictions, the transaction structure can be used interchangeably within the cash-driven and securities-driven markets. That is, securities-driven transactions can also be structured as repos, with cash-driven transactions structured as securities loans.

The securities-driven market remains more highly intermediated than the cash-driven market and transactions are more customised. Intermediaries, such as custodian banks, dealers, third-party agents and occasionally finders, are often relied upon to make markets and negotiate and price deals. The cash-driven market is more commoditised with trading at market interest rates. Counterparties often deal on a direct basis with terms for transactions displayed on electronic screens.

Both securities and cash-driven securities lending markets are an increasingly vital component of domestic and international financial markets, providing liquidity and greater flexibility to securities, derivatives and financing markets. The securities-driven market has also contributed to more efficient and less risky securities settlement arrangements. The cash-driven markets are also especially useful to central banks, both for their own monetary policy operations and as a source of information on market interest rate expectations.

2 Transaction structures

Securities lending transactions are typically structured in one of three ways: as (1) securities loan transactions; as (2) repurchase agreements; or as (3) sell-buyback arrangements. While the legal structure of the transactions differs, the economics are similar, as there is a temporary exchange of securities, typically for cash or other collateral.

2.1 Securities loan transactions.

In a typical securities loan transaction, the owner of securities lends securities to a borrower which becomes contractually obligated to redeliver a like quantity of the same security – see Figure 1. Securities borrowers are generally required to provide collateral to assure the performance of their redelivery obligation. Collateral may take the form of cash, other securities or a bank-issued letter of credit. It is standard industry practice for the lender of securities to receive initial margin that is collateral in excess of the market value of the loaned securities. This acts as a buffer against an adverse change in the price of loaned securities relative to collateral in the event that the borrower defaults on its return obligation. The lender receives a fee that is negotiated at the time of the transaction. Loans can be made on an overnight, open (terminable on demand) or term basis.

The securities lender typically does not retain legal title to the securities that are lent. The borrower obtains full title to the securities. The transaction would not be viable if the lender retained legal title to the securities it has lent, since the borrower may need legal title to the securities to transfer them to another party. Even if the securities borrower defaults on its redelivery obligation, the securities lender has no property interest in the original securities that could be asserted against any person to whom the securities borrower may have transferred them. The securities lender’s protection is its right to foreclose on the collateral.( It is important to note that, in certain markets, the rights obtained by the lender with respect to collateral may be less than full ownership.)

While the securities lender does not retain legal title to the securities that are delivered to the borrower, the lender does retain contractual rights similar to beneficial ownership, as discussed in Section 1.1 above. Meanwhile, the securities borrower is entitled to receive all economic rights of beneficial ownership of the non-cash collateral to the extent it would be so entitled if the collateral had not been transferred to the lender.

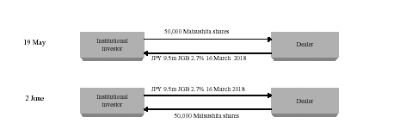

Example:

Dealer wants to borrow 50,000 shares in Matsushita Electric Industrial and will pledge Japanese government bonds (2.7 % 16 March 2018).

Dealer is willing to pay a borrow fee of 30 basis points for two weeks, 19 May 1999 to 2 June 1999. Both the borrow and pledge will settle

versus identical cash amounts with JPY 11,930 fee paid separately to institutional investor.

Calculation of collateral value required

Current market price of Matsushita JPY 2,005

Value of collateral required = value of equities borrowed (JPY 100,250,000) + 2% margin = JPY 102,255,000

Calculation of nominal amount of collateral

Current market price of the JGB (16 March 2018) 101.0340

Accrued interest as of 19 May 3.9867

All-in price 105.0207

Nominal amount of bonds required by dealer = market value of 50,000 Matsushita shares/(all-in price/100)

= 102,255,000/(105.0207/100) = JPY 9,500,000 (rounded)

Calculation of fee payment

Fee payable = nominal amount of equities borrowed * (#days borrowed/360 days)borrow fee =

102,255,000 * (14 days/360 days) * 0.0030 = JPY 11930

2.2 Repurchase agreements.

Repurchase agreements, commonly called repos, are securities lending transactions in which one party agrees to sell securities to another against the transfer of funds, with a simultaneous agreement to repurchase the same or equivalent securities at a specific price at a later date – see Figure 2. Parties borrowing securities are often referred to as buyers, while parties lending securities are referred to as sellers. While market participants may execute repo transactions to obtain control of specific securities, repos are also often structured as secured cash loans, with the repo buyer receiving securities as collateral to protect it against the cash borrower’s default.

In repo transactions, fees generally take on an interest component which is implicit in the pricing structure of the transaction. Securities are initially valued and sold at the current market price plus any accrued interest to date. At the termination of the repo transaction, the securities are resold at a predetermined price equal to the original sale price (market price + accrued interest), plus a previously agreed upon interest rate (the repo rate). In securities-driven transactions, setting the repo rate at a level lower than current money market yields will compensate the lender of securities. Even though the securities lender will be paying more to repurchase its securities, the repurchase price will account for the fact that the lender was able to invest the funds received from the initial sale in money markets at a higher rate than it was required to pay to the borrower of securities. In a cash-driven deal, the repurchase price will typically be set so that the lender of cash (securities borrower) earns the equivalent to current money market yields.

Unlike securities loan transactions, the transfer of the interest in securities from the repo seller to the repo buyer might be characterised as an outright sale or as the creation of a security interest. Repo transactions are typically structured such that all of the seller’s interest in the purchased securities passes to the buyer and that nothing precludes the buyer from selling, transferring, pledging or hypothecating the purchased securities. Unlike securities loan transactions, repo sellers may also retain the right to substitute other securities for those that were initially repoed out. This would typically only be agreed to by the counterparties in cash-driven deals where securities are serving as collateral for a secured loan.

In cash-driven repo deals, margin is often provided to the lender of money by pricing securities transferred as collateral at market value minus a “haircut”. The initial sale price is therefore less than the market value of the securities. Conversely, in securities-driven deals, the lender of securities will typically receive margin by pricing securities higher than their market value.

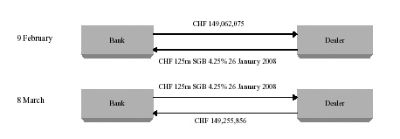

Example:

Example:

A dealer needing to raise cash for 30 days from 9 February to 8 March can provide CHF 125 million Swiss government bonds (4.25% 26 January 2008) as collateral and quotes a repo rate of 1.56%. The repurchase price will be set at CHF 149,255,856 so that the bank will earn repo interest of CHF 193,780 (see calculation below).

Calculation

Current market price 115.12373

2% haircut (2.30247)

Accrued interest as of 9 February 6.42840

All-in price 119.24966

Amount of cash provided by bank = nominal value of collateral*(all-in price/100)

125,000,000*(119.24966/100) = CHF 149,062,075

Repo interest to be paid to bank = CHF 149,062,075 * (30 days/360 days) * 1.56% = CHF 193,780

2. 3 Sell-buyback arrangements.

Market participants can also effect securities lending transactions by entering into separate sell and buy trades – see Figure 3. A key element of a sell-buyback transaction is that both the sell and buy trades are entered into at the same time, with the purchase transaction for settlement at a future date. An investment rate, typically the repo rate, is used to derive the forward contract price. In a sell-buyback, the purchaser of securities (i.e. the borrower) receives legal title and beneficial ownership of the securities. The purchaser retains any accrued interest and coupon payments during the life of the transaction. However, the end price reflects the economic benefits of a coupon being passed back to the seller.

In general, sell-buyback transactions are financing trades and limited to fixed income securities. A cash borrower does not normally have the right to substitute collateral. Sell-buyback transactions have traditionally taken place outside a fully documented legal framework (i.e. without a contract setting forth the terms and conditions linking the sale and purchase transactions); thus, margin is not provided in these transactions (i.e. flat pricing at 100% market value). Rather, trade confirmations are delivered showing the details of the trade and that there is the forward obligation to honour the agreement.

However, in 1996 PSA/ISMA introduced an annex to their Global Master Repurchase Agreement with specific provisions for sell-buyback transactions.

[The PSA/ISMA GMRA is a global master agreement for repo transactions that is used widely in international and many domestic markets. The Public Securities Association (PSA) is a bond industry trade association in the United States now known as the Bond Market Association (BMA). The International Securities Market Association (ISMA) is the selfregulatory industry body and trade association for the international securities market. The Agreement is designed for use in repo and (in jurisdictions where it is possible) sell-buyback transactions. There are several national annexes with which the Agreement may be used. Although originally drafted to cover net-paying securities only, the Agreement has recently been amended to allow it to be used for gross-paying securities, for equities (for which an additional annex is available) and for US Treasury bonds. The Agreement operates under English law. See Section 3.2 below for further discussion of the Agreement.]

Moreover, with the introduction of the Capital Adequacy Directive (CAD)5 in Europe, sell-buyback transactions do not receive a favourable capital treatment unless they are made under a legally enforceable agreement. These factors are combining to make full documentation of sell-buybacks more common.

[The EU Capital Adequacy Directive (93/6/EEC), which was adopted by the European Council on 15 March 1993, aims to harmonise prudential supervision of credit institutions and investment firms (“institutions”) authorised to operate in the European Union. In particular, it defines the own funds of institutions; sets minimum capital requirements for credit, market and settlement risk; and establishes common rules for the monitoring and control of large exposures. It also provides a common framework for supervision of institutions on a consolidated basis. EU member states may have requirements over and above those set by the Directive. The Directive applies (as with any other Community Directives) to EEA countries (EU and EFTA countries: Norway, Iceland and Liechtenstein); Switzerland took account of the basic principles of the Directive in establishing its own capital adequacy regime. See Section 3.3 for further discussion of the CAD.]

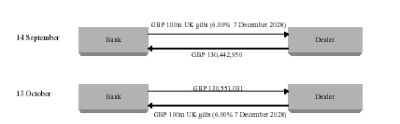

Example:

Example:

A dealer wants to borrow GBP 100 million UK gilts (6.00 %, 7 December 2028) from 14 September to 13 October. A bank quotes a rate of 5.63%.

Calculation

Pricing the buy transaction for 14 September Pricing the sellback transaction for 13 October

Current market price 128.82000 All-in buy price 130.442950

Accrued interest as of 14 September 1 .62295 (+) Repo interest .583491

All-in price 130 .44295 (-) Accrued interest as of 13 October .475410

Sellback price quoted 130.551031

Cash provided by dealer = nominal amount* (all-in price/100) =

100,000,000 *(130.442950/100) = GBP 130,442,950

Thus, dealer sells back GBP 100 million UK gilts at the predetermined price of GBP 130,551,031

“Repo” interest to be paid to bank (act/365 convention) =

130,442,950* (29 days/365 days) * 5.63% = GBP 583,491